55k After Tax UK | Your 2026 Salary and Tax Saving Guide

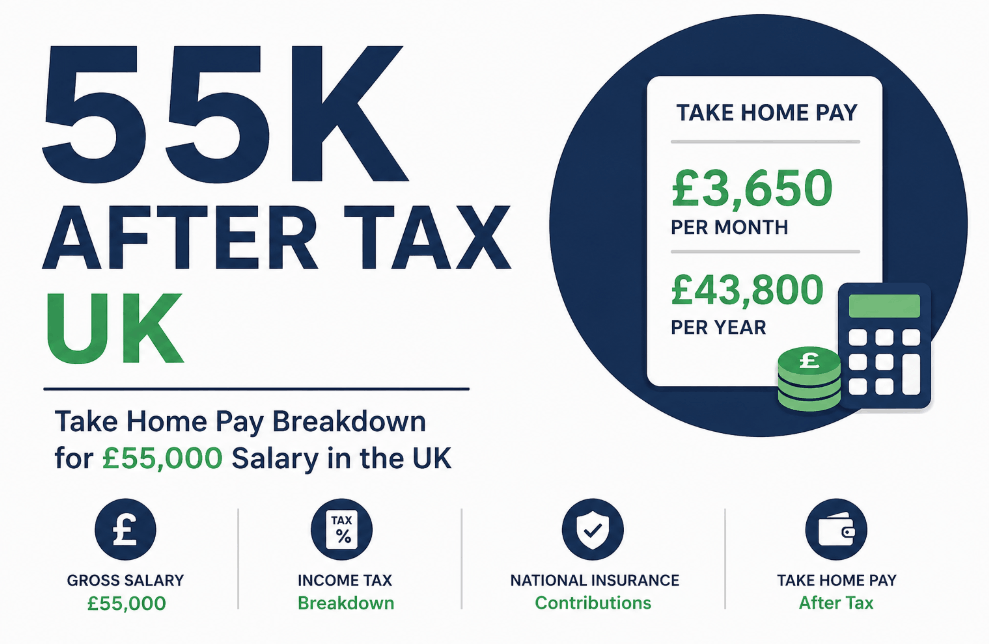

For the 2026/27 financial year, an individual earning a £55,000 gross annual salary in the UK (excluding Scotland) typically receives a take-home pay of approximately £41,560. This figure accounts for the standard £12,570 Personal Allowance, a 20% basic rate tax on earnings up to £50,270, and a 40% higher rate tax on the remaining £4,730, alongside Class 1 National Insurance contributions.

Take home pay and tax saving guide for 55k after tax UK

Earning £55,000 places you comfortably within the top 15% of UK earners, transitioning you from a basic rate taxpayer into the higher rate bracket. However, the headline figure on your contract rarely reflects the reality of your bank account once HMRC and National Insurance (NI) deductions are applied.

For those on a standard 1257L tax code, your monthly net income will hover around £3,463, though this fluctuates based on student loans, pension percentages, and taxable benefits like company cars or health insurance.

How much is 55k after tax UK in 2026?

In the UK, a £55,000 salary results in a total tax liability of roughly £13,440 per year for a standard employee. This is comprised of approximately £10,430 in Income Tax and £3,010 in National Insurance contributions.

Consequently, your monthly take-home pay is £3,463, your weekly pay is £799, and your daily rate (based on a 5-day week) sits at £160.

Many professionals reaching this level often compare their earnings to those on a 50k after tax UK bracket to see if the promotion is worth the increased tax burden.

The 2026/27 Salary Breakdown Table

| Period | Gross Income | Income Tax | National Insurance | Net Take-Home |

| Yearly | £55,000 | £10,432 | £3,008 | £41,560 |

| Monthly | £4,583 | £869 | £251 | £3,463 |

| Weekly | £1,058 | £201 | £58 | £799 |

While these figures provide a baseline, the UK tax system is rarely one size fits all. In practice, an SEO strategist or a mid-senior manager earning this amount often sees a lower net figure due to workplace pension auto-enrolment.

If your income grows toward a £65k After Tax UK level, these deductions become even more critical to manage.

Why does your 55k salary look different than others?

The most common reason for a discrepancy in take-home pay among those earning £55,000 is the tax code.

Most people are on 1257L, meaning they can earn £12,570 tax-free. However, if you have underpaid tax in a previous year or receive Benefits in Kind (BIK), your code might be lower (e.g., 1100L), increasing your monthly tax bill.

Conversely, if you have claimed tax relief on professional subscriptions or uniform maintenance, your take-home pay might increase slightly.

Student loan deductions on a 55k annual salary

If you graduated from university, your 55k after tax UK reality includes a significant deduction for student loans. Under Plan 2, you pay 9% on everything earned over £27,295. On a £55,000 salary, this amounts to roughly £2,493 per year.

This is a significant jump compared to the repayments required for a 40k after tax UK salary.

How 55k after tax UK differs in Scotland and England

It is vital to note that if you live in Scotland, your 55k after tax UK calculation will differ significantly. The Scottish Government uses a multi-tier tax system. Earning £55,000 in Glasgow involves an Intermediate Rate and a Higher Rate that kicks in earlier than in England.

Typically, a high-earner in Scotland will pay roughly £500–£800 more in annual income tax than someone in London or Cardiff on the same salary.

Living standards on a 55k salary in the UK

Statistically, £55,000 is an excellent salary. It provides enough discretionary income to support a mortgage on a property valued up to £250,000 and still allow for savings.

However, those aiming for a 80k after tax UK lifestyle often find that while the gross pay is much higher, the tax efficiency must be managed perfectly to feel the benefit.

Cost of living context for 55k earners

| Expense Category | Estimated Monthly Cost (Single) | Estimated Monthly Cost (Family of 3) |

| Housing (Rent/Mortgage) | £900 – £1,400 | £1,200 – £1,800 |

| Utilities & Council Tax | £250 | £400 |

| Groceries | £200 | £450 |

| Transport/Commute | £150 | £300 |

| Remaining Disposable | £1,463 – £1,963 | £513 – £1,113 |

For a single professional in a city like Manchester or Leeds, £3,463 a month offers a high standard of living. However, for a family in London or the South East, the high cost of childcare and housing can make £55,000 feel relatively tight, especially if it is the sole household income.

How can you increase your take-home pay on a 55k salary?

At £55,000, you have officially entered the 40% Higher Rate tax band. This means for every £1 you earn above £50,270, HMRC takes 40p in income tax. This tax cliff makes £55,000 the perfect entry point for aggressive tax planning.

By using legal financial structures, you can effectively push your taxable income back down below the threshold.

8 Steps to Optimise Your Net Income

- Increase Pension Contributions: Contributing via Salary Sacrifice reduces your gross pay, meaning you avoid the 40% tax on those funds.

- Check Your Tax Code: Ensure HMRC hasn’t assigned you an emergency code or neglected to remove a BIK you no longer use.

- Use the Cycle to Work Scheme: Purchase a bike and gear tax-free, with deductions taken from your gross salary.

- Charitable Giving: Use Gift Aid to extend your basic rate tax band, which is highly beneficial for higher-rate taxpayers.

- Marriage Allowance: If your spouse earns less than £12,570, they can transfer £1,260 of their allowance to you.

- Claim Professional Expenses: If you pay for your own professional body fees (e.g., ACCA, GMC, RCN), claim the tax back.

- Electric Vehicle (EV) Sacrifice: Lease a car through your employer; the BIK rates on EVs remain significantly lower than petrol/diesel.

- Invest in an ISA: While this doesn’t change your PAYE tax, it ensures future growth on your £55k income remains tax-free.

Maximising Pension Contributions

When reviewing financial decisions, a common pattern among high earners is the use of pension top-ups to stay out of the higher rate bracket. If you earn £55,000 and put £4,731 into your pension via salary sacrifice, your taxable income drops to £50,269.

You effectively save the 40% tax you would have paid on that £4.7k, essentially getting a 40% boost from the government on your retirement savings.

What does a 55k income look like for UK retirees?

For retired people seeking guidance on tax savings, a £55,000 retirement income is treated differently than employment income. While you still have the £12,570 Personal Allowance, retirees do not pay National Insurance.

If your £55,000 income comes from a private pension or a combination of the State Pension and a drawdown, your take-home pay will actually be higher than a worker’s. Without the £3,000 National Insurance deduction, your annual take-home pay would be approximately £44,568.

A common mistake for retirees is failing to manage drawdown amounts, potentially triggering a 40% tax bill in one month that could have been avoided by spreading withdrawals across two tax years.

Summary and Next Steps

Earning £55,000 in the UK is a significant milestone that offers financial stability but requires more active management than lower-income brackets. To maximise your 55k after tax UK income, your next steps should be:

- Audit your payslip: Ensure your tax code is 1257L and check for any unexpected Deductions.

- Calculate your pension: Use your company’s portal to see if increasing your contribution by 1–2% could save you a significant amount in 40% tax.

- Review Benefits: If you are a retiree, ensure you are utilizing your tax-free lump sum (usually 25%) strategically to stay within the basic rate bracket.

FAQ about 55k after tax UK

Is 55k considered a higher rate taxpayer?

Yes. In the UK (England, Wales, NI), the higher rate of 40% starts at £50,271. Since you earn £55,000, the top £4,729 of your salary is taxed at the 40% rate.

How much is 55k after tax monthly?

On a standard 1257L tax code for the 2026/27 tax year, your monthly take-home pay is £3,463.33. This assumes no student loans or pension deductions.

What is the hourly rate for a £55,000 salary?

Based on a standard 37.5-hour work week and 52 weeks a year, a £55,000 salary equates to approximately £28.21 per hour before tax.

Does 55k affect my Child Benefit?

Yes. The High Income Child Benefit Charge starts when one parent earns over £60,000 (as per the 2024 budget update). At £55,000, you are currently below the threshold and can keep the full benefit.

How much National Insurance do I pay on 55k?

Under current 2026 rates, you will pay roughly £3,008 per year in Class 1 National Insurance, which is deducted automatically via PAYE.

Can I get a tax refund on a 55k salary?

You may be eligible for a refund if you overpaid tax during a job change, worked only part of the year, or have unclaimed professional expenses.

Is 55k enough to live in London?

It is a middle-class London salary. While you can afford to live there, you may need to share a flat or live in Zone 3 or 4 to maintain significant savings.