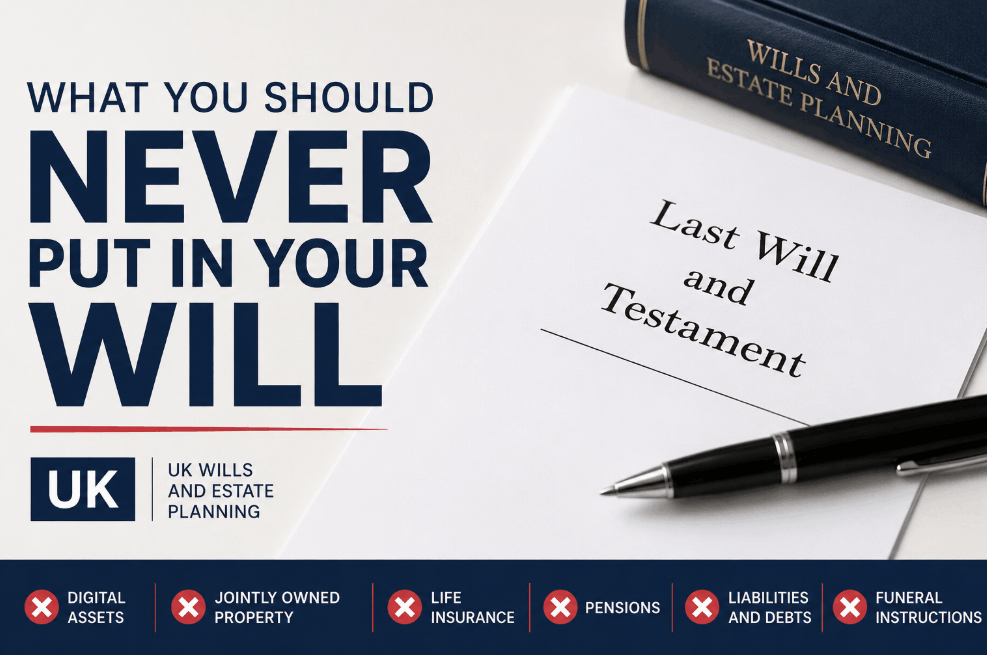

What You Should Never Put In Your Will UK: A 2026 Guide To Probate Assets, Pensions, And Taxes

What you should never put in your Will in the UK includes jointly owned property (joint tenants), pension death benefits, and life insurance policies written in trust. Because these assets pass automatically to beneficiaries outside of the probate process, including them in your Will can cause legal confusion, delays, and potential disputes for your executors.

Key Takeaways

- Non-Probatable Assets: Pensions and life insurance bypass your Will and are governed by Expression of Wish forms.

- Joint Ownership: Property held as Joint Tenants passes automatically to the survivor regardless of what your Will says.

- Privacy Concerns: Once probate is granted, your Will becomes a public document; keep sensitive data in a private Letter of Wishes.

- Timing Issues: Funeral instructions in a Will are often read too late; communicate these to your family directly.

- Illegal Conditions: You cannot include conditions that are illegal or promote immoral acts.

What You Should Never Put in Your Will UK?

To streamline probate and protect your beneficiaries from avoidable tax traps, you should omit the following assets from your Will:

- Jointly Owned Property (Joint Tenants): Under the Right of Survivorship, your share passes automatically to the surviving owner, regardless of your Will’s instructions.

- Pension Pots and Death Benefits: Most UK pensions are discretionary trusts; they are governed by your Expression of Wish form held by the provider, not your Will.

- Life Insurance Held in Trust: These policies are designed to pay out directly to beneficiaries to avoid Inheritance Tax and the delays of probate.

- Digital Passwords and Access Keys: Since a Will becomes a public document after probate, listing passwords or crypto seeds creates a significant security and identity theft risk.

- Detailed Funeral Instructions: These are often read after the funeral has occurred; a separate Letter of Wishes is the standard for timely communication.

- Business Partnership Interests: These are usually governed by a Partnership Agreement, which takes legal precedence over any personal testamentary wishes.

Assets Held in Joint Tenancy

In the UK, there is a major legal distinction between owning property as Joint Tenants and Tenants in Common. If you are Joint Tenants, you do not technically own a share that can be bequeathed; you own the whole property together.

Upon death, the property passes instantly to the survivor. Attempting to gift my half of the house in a Will when you are a Joint Tenant is a frequent cause of legal friction and will be struck out by the Probate Registry.

Pension Death Benefits

Most modern UK pensions are structured as discretionary trusts to keep them outside of your estate for Inheritance Tax purposes. This means the pension trustees have the final say on who receives the funds. They will almost always follow your Expression of Wish (Nomination) form.

If you try to override this in your Will, you create a conflict that forces executors into lengthy correspondence with pension providers, often delaying the payout for months.

Life Insurance Policies Written in Trust

If a life insurance policy is written in trust, the proceeds are not part of your legal estate. The primary benefit of this is speed; the insurance company can pay the beneficiaries immediately without waiting for a Grant of Probate.

Mentioning these specific funds in your Will is unnecessary and could prompt HMRC to investigate assets that should have otherwise remained tax-exempt. Similarly, avoid void conditions, instructions that are illegal or against public policy, as these are often struck out by the courts.

Funeral Wishes and Immediate Instructions

Including funeral instructions in a Will is often a wasted effort. Since Wills are rarely located or read until weeks after the passing, these wishes are frequently discovered only after the ceremony has taken place.

The process of locating the Will and getting it read often happens after the funeral arrangements have already been settled.

To ensure your wishes are followed, it is better to provide your family with a Letter of Wishes, a separate, non-public document that can be opened immediately upon your passing.

Sensitive Digital Information

Once probate is granted, your Will becomes a matter of public record. Anyone can pay a small fee to the government to see a copy of it.

Therefore, you should never include bank PINs, login credentials, or private encryption keys within the text. Instead, use a secure digital legacy tool or leave instructions in a private file for your executors to find.

Illegal or Unenforceable Conditions

English law generally respects testamentary freedom, but this has limits. You cannot include conditions that are illegal or contrary to public policy.

For instance, a gift that is only triggered if a beneficiary changes their religion or divorces their partner is likely to be challenged in court. These conditions are often deemed void for uncertainty or void for immorality, leading to expensive litigation that depletes the estate’s value.

Why are certain assets legally excluded from a UK Will?

Not everything you own in a daily sense is yours to give away in a will. The UK recognizes distinct legal structures that bypass the probate process entirely to ensure a faster transfer of funds or property to survivors.

While this guide focuses on intentional exclusions, many people often wonder what happens to bank account when someone dies without a will UK.

In such cases, the rules of intestacy take over, which is exactly the lack of control that a well-drafted Will, and a clear understanding of non-probatable assets, aims to prevent.

How Joint Property Ownership Overrides a Will

If you own your home as ‘Joint Tenants’ with a spouse or partner, the property passes automatically to them upon your death. Because this happens by law, any mention of the property in your Will is legally redundant; you simply do not have a transferable ‘share’ to leave to anyone else while the other tenant is alive

Pensions and Life Insurance Trust Arrangements

Most modern UK pensions are held under a discretionary trust. Because the funds are technically held by the pension trustees, they do not form part of your legal estate for Inheritance Tax (IHT) purposes.

A common mistake is attempting to nominate pension beneficiaries within a Will. In practice, pension trustees usually prioritise the Nomination of Beneficiaries form held on their own systems, meaning your Will’s instructions could be entirely bypassed, leading to confusion for your executors.

Business Property Relief (BPR) and 2026 Changes

As of the 2026/27 tax year, the UK government has implemented a £1 million cap on combined 100% relief for Business and Agricultural assets.

When reviewing decisions regarding business succession, placing specific business assets in a will without considering the new 2026 IHT thresholds can lead to a massive, unexpected tax bill for your heirs.

These complexities are amplified during long-term estate planning, particularly when calculating inheritance tax when second parent dies. At this stage, the combined value of property, business assets, and unused allowances from the first spouse must be carefully managed to stay within the latest legal limits.

| Asset Type | Included in Will? | Why / Why Not? |

| Sole Bank Accounts | Yes | Forms part of your legal personal estate. |

| Joint Bank Accounts | No | Passes automatically to the surviving account holder. |

| Life Insurance (In Trust) | No | Paid directly to beneficiaries to avoid IHT and probate. |

| Personal Possessions | Yes | Known as chattels, specifically distributed by the will. |

| Pensions | No | Governed by the provider’s Expression of Wish form. |

| Property (Tenants in Common) | Yes | You own a specific share that can be bequeathed. |

What are the risks of including funeral wishes in a will?

It is a common misconception that the will is the best place for funeral instructions. In reality, the will is often not located or read until several weeks after a person has passed away—frequently after the funeral has already taken place.

- Locate your Will: Ensure it is with a solicitor or the National Will Archive.

- Draft a Letter of Wishes: Create a separate, non-legally binding document for funeral details.

- Appoint Executors: Choose people who are aware of your funeral preferences.

- Discuss Digital Assets: Use a secure password manager rather than listing codes in a will.

- Review Joint Titles: Check if your home is held as Joint Tenants or Tenants in Common.

- Update Nominations: Ensure your pension and life insurance forms match your current intent.

- Address the 2026 IHT Cap: If you own a business, consult a specialist regarding the £1m relief limit.

Can you leave conditions on gifts in a UK Will?

While you can technically add conditions to a gift (e.g., to my son provided he graduates from university), Dead Hand Control is often frowned upon by UK courts. Any condition that is considered contrary to public policy, such as requiring someone to divorce or change their religion, will likely be ruled invalid.

A common pattern is trying to prevent a beneficiary from selling a house. Instead of a complex condition in the will, legal experts often suggest a Life Interest Trust. This allows someone to live in the property for their lifetime, while the underlying value is protected for the ultimate beneficiaries.

This provides the control you desire without the risk of the clause being challenged for being too restrictive or uncertain.

How do digital assets impact your will in 2026?

Modern UK estates now frequently involve ‘invisible’ assets like cryptocurrency, social media accounts, and cloud storage. However, you should never put passwords, PINs, or private keys directly into your will.

Privacy and Security Risks

Once probate is granted, your will becomes a public document. Anyone can order a copy from the government for a small fee. If you have listed the combination to a physical safe or the password to a Bitcoin wallet, you have effectively handed that information to the public.

Managing Your Digital Legacy Securely

Instead of listing specifics, include a general clause giving your executors the power to manage digital assets. Use a separate, secure Digital Legacy document or a password manager’s emergency access feature to ensure the right people get the right codes at the right time.

Why you should avoid leaving gifts to pets in a Will?

Under UK law, animals are classified as property and cannot legally own assets or cash themselves. You cannot leave £5,000 to my cat, Whiskers.

The Correct Approach:

A more effective strategy is to leave the pet, along with a maintenance legacy (a sum of money), to a trusted friend or a charity like the RSPCA or Dogs Trust. Include a request in your Letter of Wishes detailing the pet’s diet and care requirements. This avoids the gift failing for lack of a legal recipient.

Summary and Next Steps

Writing a will is about clarity and legality, not just sentiment. To ensure your estate is handled efficiently:

- Remove any assets that pass by survivorship or nomination (pensions/life insurance).

- Move personal messages and funeral plans to a Letter of Wishes.

- Consult an expert if you have business assets exceeding £1 million to navigate the 2026 IHT reforms.

- Keep the document focused on who gets what of your personal legal estate.

FAQ

Can I put my bank account passwords in my will?

No. A will becomes a public record after probate. Listing passwords or PINs exposes your accounts and digital identity to fraud. Use a separate, secure Letter of Wishes for sensitive data.

What happens if I include a jointly owned house in my will?

If held as Joint Tenants, the house passes automatically to the survivor regardless of what the will says. The clause in your will would be legally ineffective and ignored.

Why shouldn’t I include funeral wishes in my will?

Wills are often read after the funeral. It is better to tell your executors directly or keep a Letter of Wishes in an accessible place to ensure your preferences are met.

Can I leave money to a political party in my will?

Yes, but you should ensure the wording is precise. However, avoid including long political manifestos or reasons for the gift, as these can be contested or cause public embarrassment.

Does my income tax personal allowance affect my Will?

No. While your 1257L code determines your tax-free income while you are alive, Inheritance Tax (IHT) is a separate calculation based on your total estate value against the £325,000 Nil Rate Band.

Can I leave a gift to a witness of my will?

No. Under the Wills Act 1837, any gift made to a person who witnesses the will (or their spouse) is automatically void. The rest of the will remains valid, but that person gets nothing.

Should I list my specific debts in my will?

It is unnecessary. Your executors are legally required to pay your valid debts from the estate assets before distributing gifts. Listing them just clutters the document and may become outdated.

Is it okay to exclude an estranged child from my will?

You can, but you must be careful. In the UK, the Inheritance (Provision for Family and Dependants) Act 1975 allows certain people to claim against an estate if they weren’t reasonably provided for.