HMRC State Pension Tax Error: How to Spot Tax Code Faults and Correct Overpayments?

The HMRC state pension tax error refers to a systemic failure to properly synchronise historical National Insurance records and benefit pay-outs between the DWP and HMRC. Because the state pension is paid gross, the system alters PAYE codes on secondary incomes to collect tax, frequently triggering excessive, incorrect deductions.

An administrative misalignment between the Department for Work and Pensions (DWP) and HM Revenue and Customs (HMRC) means hundreds of thousands of UK retirees are facing incorrect tax bills.

What is the HMRC State Pension Tax Error?

The HMRC State Pension Tax Error refers to two systemic failures: a nine-year digital glitch in the online Check your State Pension tool (corrected in February 2026) that issued inflated forecasts to 800,000 people, and an ongoing data-sync failure between the DWP and HMRC that applies incorrect PAYE codes to retirees’ secondary incomes.

The 2016–2026 Online Forecast Tool Glitch

The true scale of the system misalignment became clear on February 13, 2026, when HMRC implemented an urgent system update to correct a major nine-year technical flaw within its online State Pension forecast tool.

Since its launch in February 2016, this digital calculator has completely failed to factor in manual adjustments for individuals who had contracted out of the Additional State Pension (SERPS or S2P) into private or workplace schemes before April 2016.

Consequently, the tool issued inflated forecasts to roughly 800,000 citizens. Many based early retirement choices, State Pension Deferral strategies, or voluntary National Insurance (NI) top-up plans on flawed data, only to find their actual payouts lower than expected or their tax profiles severely distorted.

Ongoing DWP and HMRC Data Sync Mismatches

Beyond the historical forecasting glitch, real-time operational data mismatches continue to disrupt personal finances. When the DWP updates an individual’s gross annual award under the Triple Lock mechanism, HMRC’s central PAYE system frequently duplicates values or applies outdated historical deduction codes.

If a retiree holds a part-time job or draws a private occupational pension, HMRC frequently applies an incorrect tax code to that secondary source, triggering excessive tax deductions.

What is the HMRC Pension Tax Warning?

Under the Income Tax (Earnings and Pensions) Act 2003, all pension income is classified as taxable earnings. While the full New State Pension has climbed to £241.30 per week (equivalent to £12,547.60 per year) under the Triple Lock, the UK Personal Allowance remains aggressively frozen at £12,570.

The core issue behind the widely reported HMRC pension tax warning is fiscal drag, a phenomenon heavily impacting small business owners, retired company directors, and standard savers alike.

- The Baseline: The full New State Pension stands at £12,547.60 per year, which effectively consumes 99.8% of your entire tax-free allowance.

- The Tax Trigger: Because your allowance is almost entirely used up by the state pension, any secondary income, regardless of the amount, immediately breaches the threshold. This includes income from a private pension, a part-time job, or business dividends.

- The Outcome: Once that secondary income pushes you past the £12,570 cap, the additional funds are subject to standard income tax rates of 20% or 40%. This tax is collected either automatically through a secondary PAYE income stream or retroactively via an HMRC Simple Assessment (Form PA302).

Why is the State Pension Tax Error Happening?

The fundamental reason the state pension tax error is happening boils down to an architectural mismatch between two entirely different government computer networks. The DWP tracks benefit payouts on an entirely separate database from HMRC’s central Pay As You Earn (PAYE) database.

Because the state pension is paid legally gross (without tax deducted at source), HMRC is forced to manually or digitally load your state pension amount as an asset onto your secondary income streams to slash your tax-free allowance.

When the DWP scales up your pension via the Triple Lock every April, the API software running between the two departments often fails to sync the changes in real-time, resulting in duplicated values, dropped data packets, or flat-out wrong code configurations.

How Does the HMRC State Pension Tax Error Affect UK Retirees?

The HMRC state pension tax error affects UK retirees by triggering severe, unexpected reductions in their monthly disposable cash flow. Because tax cannot be deducted directly from state benefits, HMRC forces secondary pension providers to slash personal allowances, inadvertently plunging thousands into emergency tax brackets.

The Financial Cascade Effect

- Immediate Income Diminution: Under the Income Tax (Earnings and Pensions) Act 2003, data discrepancies force HMRC to adjust your PAYE coding notice, legally mandating your private pension provider to slash your tax-free allowance.

- Retroactive Tax Bills: For retirees whose total income barely breaches the frozen £12,570 threshold, HMRC issues a Simple Assessment (Form PA302), demanding unexpected back-payments.

- Artificial Bracket Inflation: Inaccurate K codes turn your state pension into a negative asset. If you withdraw a flexible private pension lump sum, automated systems apply an emergency month-one tax calculation, locking up thousands of pounds of retirement capital.

How Much Tax is Taken Off My Pension Income?

In the UK, a pension is legally classified as deferred earned income. It does not qualify for exemptions from income tax, meaning it is subject to standard tax bands once your total aggregate income exceeds your available Personal Allowance.

Crucially, there are no age-related exemptions or unique income tax bands for retirees over 70, nor is there a separate tax-free limit for older age groups in the UK. Everyone, regardless of age, shares the exact same baseline Personal Allowance framework.

Once your state pension, private occupational pensions, and any employment earnings are combined, the total sum is taxed according to standard UK Income Tax bands:

| Tax Band | Total Income Threshold | Income Tax Rate |

| Personal Allowance | Up to £12,570 | 0% |

| Basic Rate | £12,571 to £50,270 | 20% |

| Higher Rate | £50,271 to £125,140 | 40% |

| Additional Rate | Over £125,140 | 45% |

Note: Income tax bands vary slightly for taxpayers residing in Scotland.

In practice, if your state pension amounts to £11,500 and you draw an additional £10,000 from an executive workplace pension, your total income is £21,500. After subtracting your £12,570 Personal Allowance, the remaining £8,930 is taxed at the Basic Rate of 20%, resulting in a total annual liability of £1,786.

Contextualising the Age 70 Exemption Myth

There is a common misconception among taxpayers regarding age-related exemptions. Crucially, there are no age-related exemptions or unique income tax bands for retirees over 70, nor is there a separate tax-free limit for older age groups in the UK.

Everyone, regardless of age, shares the exact same baseline Personal Allowance framework.

| Myth | Reality | Official Framework |

| Retirees over 70 stop paying tax on their state pension. | All state pensions remain fully taxable regardless of the recipient’s age. | Income Tax (Earnings and Pensions) Act 2003 |

| Older pensioners receive a higher personal tax-free allowance. | Everyone in the UK shares the exact same standard Personal Allowance. | Finance Act statutory thresholds (£12,570) |

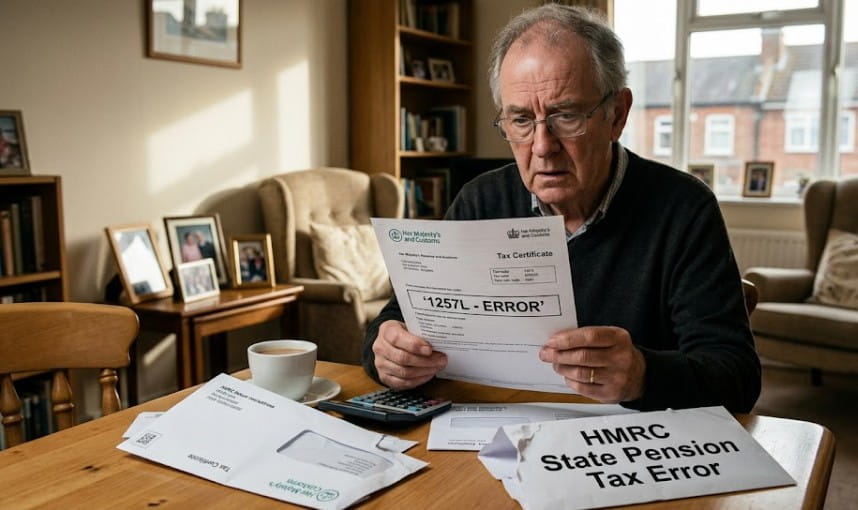

How Do You Check If Your State Pension Tax Code is Wrong?

If you maintain an active salary as an SME director or receive regular private pension pay-outs alongside your state benefit, you must carefully monitor your PAYE Coding Notice. HMRC uses this notice to instruct your company payroll or pension provider on how much tax to deduct.

To determine if your tax code has been corrupted by an administrative error, look out for distinct technical indicators:

- The Suffix L Over-Deduction: If your code is listed as 1257L on your private pension payslip while you are also receiving a state pension, the system is malfunctioning. It is accidentally giving you a double tax-free allowance, which will result in a heavy back-tax demand later. Conversely, if the code is severely reduced (e.g., 107L), verify that the exact reduction matches your actual gross state pension value down to the penny.

- The Presence of a K Code: A K tax code occurs when your untaxed income (the state pension) is higher than your total tax-free Personal Allowance. Essentially, it turns your tax code into an asset that adds taxable value to your other income streams. If HMRC overestimates your DWP benefit, the K code will result in excessive tax deductions from your primary company salary.

- BR and 0T Flat-Rate Overrides: If your secondary payslip suddenly displays BR (Basic Rate flat 20%) or 0T (no allowance split), the system may have lost track of your personal allowances entirely, forcing you into emergency tax bands.

While keeping track of the UK State Pension Age Increase 2026 timeline allows for unlimited employment or self-employment earnings, every pound of extra income alters how your tax codes are split across multiple streams.

How Much Tax Will I Pay If I Draw All My Pension or Take a Lump Sum?

Under current UK statutory rules, you are entitled to take a 25% tax-free lump sum from your private defined contribution or personal pension pots, up to a strict lifetime maximum cap of £268,275. This specific portion is entirely exempt from income tax.

However, severe financial penalties occur if you decide to withdraw the remaining 75% all at once, or in large, unscheduled chunks. Pension providers operate under strict HMRC mandates that require them to apply an emergency month-one tax code to single, large cash withdrawals.

The automated system treats a single large withdrawal as if it will be paid consistently every single month of the year.

For instance, if you withdraw a remaining £45,000 pot in one go, the PAYE system calculates tax as if your annual income is over £540,000, immediately pushing you into the 45% Additional Rate band for that specific month.

While you can claim this overpaid emergency tax back, the administrative lag can tie up your retirement capital for months.

Do HMRC Automatically Refund Overpaid Tax on pensions?

No, HMRC does not always automatically refund overpaid tax on multi-source pension errors. While the system attempts to automatically reconcile accounts at the close of the financial year via the P800 tax calculation system, data sync issues with the DWP frequently carry errors forward unless you actively intervene.

To secure your money and trigger an HMRC State Pension Tax Refund, you must navigate a defined, step-by-step correction process:

- Locate your formal DWP annual pension increase notification letter to find your exact gross entitlement.

- Log in to your official HMRC Personal Tax Account via the Government Gateway portal using a secure photo ID verification.

- Compare the DWP State Pension figure listed in your HMRC digital account against your actual bank deposits.

- If a discrepancy exists, use the Update Income Details feature to manually correct the estimated state pension value.

- If you have already suffered an emergency tax over-deduction on a private pension lump sum, download and complete Form R40 (or Form P55/P53, depending on the withdrawal type).

- Submit the form digitally or by post to trigger a manual payroll review and secure your HMRC State Pension Tax Refund.

- Monitor your online account for the formal P800 calculation sheet confirming the exact refund amount due.

Resolving an HMRC state pension tax error means taking proactive control of personal tax accounts for UK retirees in 2026.

How to Avoid and Correct the HMRC State Pension Tax Error?

To avoid and correct the HMRC state pension tax error, you must actively reconcile your annual DWP award letter with your HMRC online account. Manually updating any data discrepancies via your Personal Tax Account and auditing your PAYE coding notices ensures HMRC does not issue incorrect tax demands.

Protect your retirement income from systemic errors by filtering down from broad institutional oversight to targeted individual adjustments:

- Reconcile Broad Data (Top Base): Ensure the gross weekly figure on your physical DWP annual pension increase letter matches the State Pension Income figure displayed on your HMRC Government Gateway portal exactly. A one-penny discrepancy can trigger automatic over-taxation.

- Track Processing Signals (Middle Tier): Audit every PAYE Coding Notice sent to your employers or private pension providers. Watch for sudden structural anomalies, specifically unexpected K codes, emergency 0T codes, or unadjusted 1257L markers.

- Execute Direct Corrections (Needle Tip): Bypass automated end-of-year batch loops if an error occurs. Instantly log into your portal to use the Update Income Details feature or file Form R40 for immediate manual review.

What Are the Biggest Mistakes People Make When Retiring?

SME owners, directors, and self-employed professionals frequently stumble when transitioning into retirement because their income models are inherently more complex than those of standard PAYE employees.

Navigating the transition has become even more challenging due to the legislative timeline of the DWP State Pension Age Change 2026, which is gradually increasing the state pension age from 66 to 67.

This shifting timeline alters when people can first claim their state benefits, complicating long-term cash flow and tax planning.

Mismanaging Tax Timing on Back-Dated Pension Arrears

Consider a retired director who received an unexpected £10,000 lump-sum back-payment from the DWP due to a historic system error regarding missing National Insurance credits.

HMRC’s automated system initially attempted to tax the entire lump sum within the current financial year.

This error was costly; the lump sum artificially pushed the director into a higher tax bracket for that year. In reality, state pension arrears must legally be allocated back to the specific tax years in which they should have been paid.

HMRC is only legally permitted to collect income tax on these arrears for the current tax year and the preceding four tax years.

Mid-Year Retirement Code Crashing

Many individuals choose to retire and draw down their pension pots midway through a financial year in which they have already drawn a substantial salary or dividend income from their business.

This front-loaded income quickly absorbs their Personal Allowance, meaning their initial pension distributions are hit with heavy, unexpected emergency tax rates.

Summary and Next Steps

Correcting an administrative tax error requires quick, proactive management of your personal tax records.

Do not assume the automated systems will seamlessly align data between the DWP and HMRC networks. To safeguard your retirement cash flow, take these immediate actions:

- Log in to your Government Gateway portal to audit the specific State Pension figure HMRC has listed.

- Cross-check your private pension payslips for erratic K codes, BR codes, or unexpected changes to your standard allowances.

- If an error is spotted, upload your actual DWP award documentation through your online account or file an official manual claim using Form R40 without delay.

Verified against official HMRC 2026/27 Personal Allowance Schedules and DWP Legislative Guides.

FAQ

Why is there a state pension error occurring now?

A systemic nine-year digital glitch in HMRC’s online forecasting tool miscalculated contracted-out National Insurance records for 800,000 savers, while ongoing data mismatches between DWP payout tracking and HMRC PAYE codes cause widespread monthly over-taxation.

What is the maximum a pensioner can earn before paying taxes?

The maximum an individual can receive tax-free across all income streams combined is £12,570 per year. Once your gross state pension and alternative earnings breach this threshold, standard income tax applies.

Does my UK state pension count as taxable income?

Yes, the state pension counts entirely as taxable earned income. Although the DWP pays the benefit gross without deducting tax at the source, the total amount is paired against your Personal Allowance limit.

Can I take a tax-free lump sum from my pension every year?

You can take 25% of your pension pot tax-free, either as a single one-off lump sum or through smaller, phased cash withdrawals (UFPLS) where 25% of each individual slice is distributed tax-free.

What happens to my tax code if I receive a K code?

A K code indicates that your untaxed income, such as your state pension, exceeds your Personal Allowance. This code forces your employer or private pension provider to deduct extra tax from your remaining active income streams.

How do I fix a discrepancy between DWP and HMRC figures?

Log in to your HMRC Personal Tax Account via the Government Gateway portal, navigate to the income tracking section, select your state pension source, and use the digital portal to submit your correct DWP award figure.