DWP Pension Bank Rules Update 2026: Are Your Savings Safe?

As of March 2026, the DWP pension bank rules update introduces automated data matching via the Public Authorities (Fraud, Error and Recovery) Act.

Banks are now required to flag accounts receiving means-tested benefits, such as Pension Credit, that breach capital limits or residency rules. These automated checks do not apply to the standard State Pension.

What are the new DWP bank account checks for 2025 and 2026?

The current landscape of UK welfare oversight has shifted from manual investigation to proactive digital verification.

This shift towards digital oversight aligns with broader administrative adjustments, including the recent DWP pension payment schedule change, as the Department moves away from legacy manual processing.

Under the Public Authorities (Fraud, Error and Recovery) Act 2026, the Department for Work and Pensions (DWP) has implemented a system where financial institutions must monitor accounts for specific eligibility indicators.

The 2026 DWP bank account checks involve banks scanning their own datasets for accounts receiving means-tested benefits that exceed capital thresholds (usually £16,000) or show extended overseas spending.

Banks then issue an Eligibility Verification Notice (EVN) to the DWP, highlighting the discrepancy without sharing full transaction histories or personal shopping habits.

Understanding the Eligibility Verification Measure (EVM)

The core of this update is the Eligibility Verification Measure. Unlike previous years, where the DWP required reasonable suspicion to request bank statements, the 2026 rules allow for a test and learn automated approach.

This means the bank’s software identifies the issue, such as a balance staying consistently above £16,000 for a Universal Credit claimant, and sends a digital flag to the DWP.

- Routine Monitoring: Banks scan for balance levels and foreign transactions.

- Data Minimisation: The DWP does not see your daily coffee spend or specific retailers.

- Human Oversight: A DWP official must review every automated flag before any benefit is suspended.

Does the DWP check bank accounts for the State Pension?

Confusion often arises regarding who exactly falls under the scope of these new 2026 bank rules. In reality, the vast majority of UK retirees remain unaffected because the State Pension itself is not a means-tested benefit.

Why the New State Pension can feel unfair to existing pensioners

The 2026/27 tax year has highlighted a growing divide. Public debate continues to intensify over how the new state pension unfair to existing pensioners highlighting the growing divide between those on the Old Basic system and those who reached pension age after April 2016.

This creates a surveillance trap: because the Basic State Pension is lower, older retirees are more likely to claim Pension Credit.

Since Pension Credit is means-tested, these older pensioners find their bank accounts subject to the new 2026 monitoring rules, while wealthier retirees on only the New State Pension remain unmonitored.

| Feature | Basic State Pension (Pre-2016) | New State Pension (Post-2016) |

| 2026 Weekly Rate | £184.90 (Basic) | £241.30 (Full) |

| Means-Tested? | No | No |

| Bank Monitoring? | No | No |

| Requires Pension Credit? | Often Yes (triggers monitoring) | Rarely (avoids monitoring) |

While the pension triple lock ensures that base rates continue to rise, the increase in value does not exempt claimants from means-testing if they require additional support.

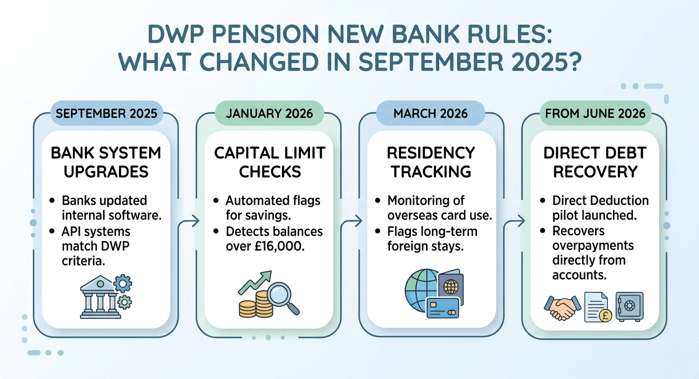

DWP Pension new bank rules: What changed in September 2025?

The transition began in earnest during late 2025, when the first Eligibility Verification Notices were served to the UK’s largest Big Five banks. This period marked the end of the pilot phase and the beginning of the live data-sharing era.

- September 2025: Banks upgraded internal API systems to match DWP eligibility criteria.

- January 2026: Rollout of automated flags for capital limit breaches over £16,000.

- March 2026: Introduction of residency tracking via overseas ATM and card usage.

- April 2026: Full integration of HMRC income data with bank balance flags.

- June 2026: Launch of the Direct Deduction pilot for debt recovery.

- Late 2026: Expansion of the scheme to include medium-sized building societies.

DWP Universal Credit bank account checks: Top 5 most common errors

Automated systems are not infallible. A significant technical hurdle involves automated scans misidentifying previous DWP cost-of-living payment instalments as undeclared savings or regular monthly income.

- Cost of Living Residuals: Older Cost of Living payments being misidentified as regular savings.

- Help to Save Overlap: The system failing to discount the tax-free bonuses in Help to Save accounts.

- Joint Liability: Flagging the full balance of a joint account against a single claimant.

- Timing Offsets: Flagging a balance the day after a monthly salary or pension is paid in, before bills are deducted.

- Redundancy Pay: Not accounting for the grace period sometimes applied to redundancy lump sums.

Navigating 2026 Surveillance

The £10,000 Deeming Rule and the £16,000 Cap

While £16,000 is the hard limit for benefit cessation, many are unaware that having savings between £10,000 and £16,000 reduces your weekly payment through notional income calculations. The 2026 update makes this tracking instantaneous.

Inheritances and One-off Gifts

Retirees frequently encounter issues when receiving one-off lump sums or inheritances. Specific arrears or supplements, such as the DWP £750 payment boost June 2025, require clear documentation to prevent them from being incorrectly flagged as recurring capital during a bank audit.

In the past, this might have gone unnoticed for months; today, the bank flag will likely reach the DWP within one statement cycle.

The 12-Month Lookback

How far back do the new scans go? Currently, the automated system looks at 12 months of historical balance data to identify deprivation of capital, the act of giving money away specifically to stay below the £16,000 limit.

Overseas Spending and Foreign Travel

If you receive Pension Credit, you must generally stay in the UK. The new rules allow banks to flag when a UK-issued card is used exclusively abroad for more than 4 consecutive weeks.

The Human in the Loop Promise

Legally, a machine cannot stop your money. If an EVN flag is raised, a DWP case officer must contact you to ask for an explanation before any Direct Deduction or suspension occurs.

Can the DWP take money without a court order?

One of the most significant powers granted in 2026 is the ability for the DWP to recover debt directly. Previously, they required a court order to garnish bank accounts. Now, if an overpayment is confirmed and a claimant refuses a repayment plan, the DWP can issue a Direct Deduction Order to your bank.

Steps for DWP Debt Recovery in 2026:

- Identification of overpayment via bank flag or HMRC data.

- Issuance of a Notification of Debt letter to the claimant.

- 30-day window for the claimant to appeal or set up a plan.

- Mandatory Reconsideration review if the debt is disputed.

- Application of a Direct Deduction Order if no agreement is reached.

- Automatic withdrawal of a set percentage from the bank account.

- Final right to appeal at an Independent Tribunal.

How to stay compliant: Updating your details

To avoid a false flag, ensure your information is accurate. You can use the DWP change of address online service or notify them of capital changes immediately.

Official DWP Support and Documentation

- Pension Service: 0800 731 0469

- Universal Credit Helpline: 0800 328 5644

- Forms: You can download the BR2102 bank details form directly from the GOV.UK portal if you need to update your payment information by post.

Summary and Next Steps

The 2026 updates represent a shift toward a digital-first welfare state. With the latest DWP benefit fraud crackdown measures now deeply embedded within the UK’s financial infrastructure, maintaining transparent and up-to-date records is essential for anyone receiving means-tested support.

For most, the message is simple: transparency is your best defence. If your savings fluctuate near the £10,000 or £16,000 marks, keep meticulous records of large transactions. If you receive an inquiry letter, respond within the 14-day window to prevent an automated suspension.

FAQ about DWP pension bank rules update

Can the DWP see what I buy at the supermarket?

No. The 2026 regulations strictly prohibit banks from sharing transaction-level data. The DWP only receives indicators, such as your total balance or the fact that a card was used abroad.

Will my bank tell me if they’ve been served an EVN?

Banks are generally not required to notify you the moment a flag is sent, but the DWP must contact you before taking any action that affects your payments.

Does the DWP check my partner’s bank account?

If you claim as a couple, both accounts are subject to the £16,000 capital limit and may be monitored. If you claim as a single person, a non-claiming partner’s account is usually private unless fraud is suspected.

How many years of bank statements can they ask for?

While the automated scan is usually 12 months, if a formal fraud investigation is opened, the DWP can legally request up to 6 or 12 years of financial records.

What happens if my account is flagged by mistake?

You should immediately provide bank statements showing the nature of the funds. You have the right to a Mandatory Reconsideration if the DWP makes an adverse decision based on a flag.

Is the State Pension taxable in 2026?

Yes. Because the full New State Pension (£12,547.60) is now nearly equal to the frozen Personal Allowance (£12,570), almost any other income (private pension or savings interest) will trigger a tax bill.

Can I hold cash to avoid the 2026 bank checks?

While not illegal to hold cash, hiding capital to remain eligible for benefits is considered benefit fraud. If the DWP sees large withdrawals that aren’t accounted for, they may assume you still possess that capital.