DWP Bank Account Deductions: 2026 Rules on Monitoring, Limits, and Your Rights

As we enter the 2026/27 tax year, the relationship between the Department for Work and Pensions (DWP) and your bank account has fundamentally changed. Following the full implementation of the Public Authorities (Fraud, Error and Recovery) Act 2025, the DWP now possesses the most significant debt recovery and monitoring powers in its history.

However, alongside these “snooping” powers, new legal protections—specifically the 15% Fair Repayment Rate—have been introduced to prevent claimants from falling into extreme financial hardship.

Quick Summary: The 2026 Status Quo

- The 15% Cap: Most DWP debt deductions are now capped at 15% of your Universal Credit Standard Allowance (down from 25% in previous years).

- Direct Deduction Orders (DDOs): For the first time, the DWP can take money directly from your bank account without a court warrant if you are no longer on benefits.

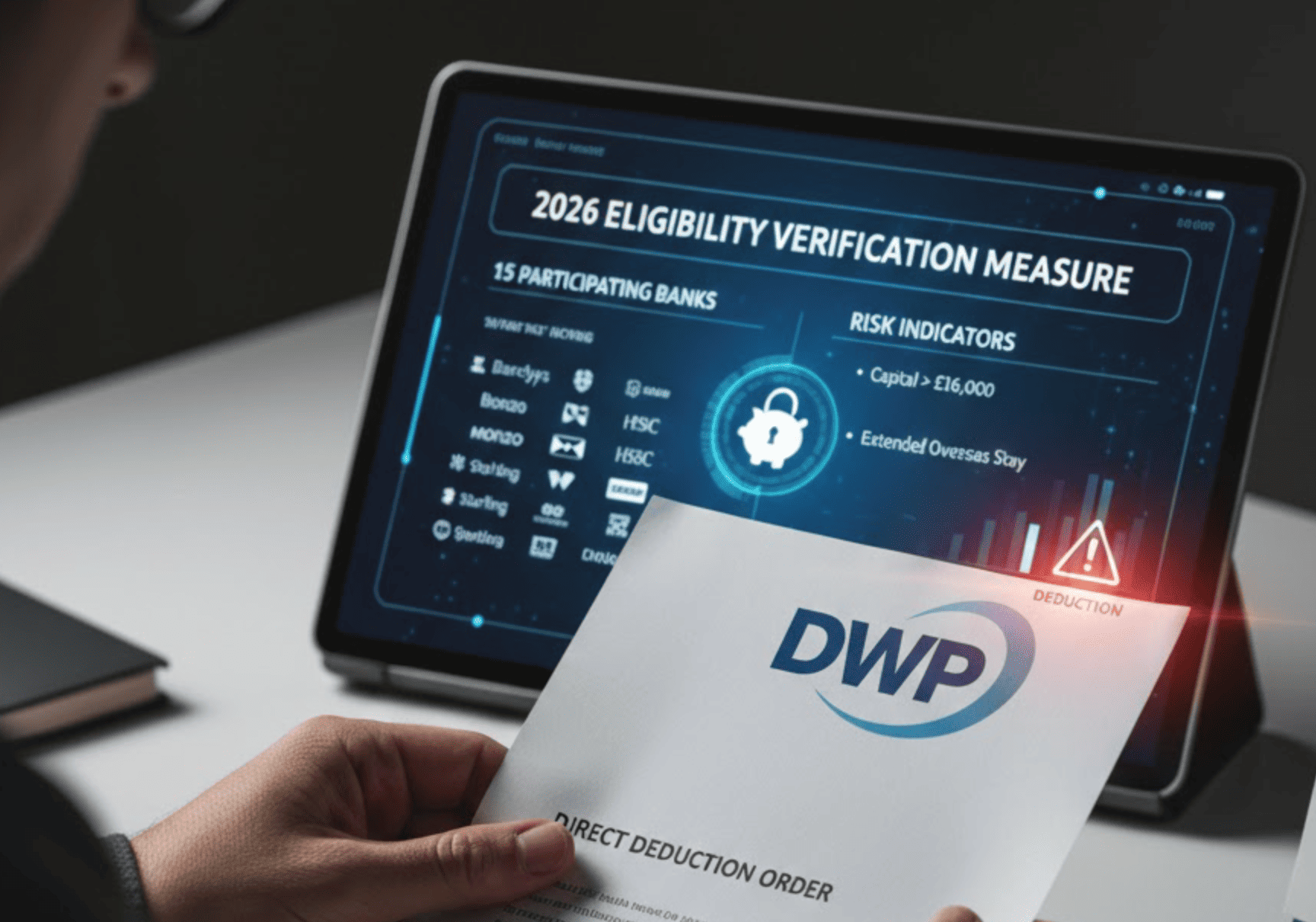

- Bank Monitoring: 15 major UK banks (including Monzo, Barclays, and HSBC) are now legally required to flag accounts that exceed capital limits or show evidence of overseas stays.

- The Driving Licence Rule: In extreme cases of “wilful” non-payment, the DWP can now apply to a court to suspend your driving licence.

1. How much can the DWP legally deduct from your benefits?

In April 2025, the government introduced the Fair Repayment Rate. For 2026, this remains the gold standard for protection.

The DWP can deduct money from your monthly payment to recover “advance payments,” overpayments, or third-party debts (like rent arrears). However, for the majority of claimants, the total deduction is capped at 15% of your Standard Allowance.

Exceptions to the 15% Cap:

- Fraud Overpayments: If the DWP has proven fraudulent intent, they can still deduct up to 25%.

- Last Resort: Deductions for ongoing consumption of water or fuel (not arrears) can sometimes push the total slightly higher if deemed in your “best interest.”

2. 2026/27 Maximum Deduction Rates

The following table shows the maximum monthly amount the DWP can deduct under the 15% cap based on the new 2026/27 benefit rates:

| Claimant Category | 2026/27 Standard Allowance (Monthly) | Max 15% Monthly Deduction |

| Single (Under 25) | £338.58 | £50.79 |

| Single (25 or over) | £424.90 | £63.74 |

| Couple (Both Under 25) | £528.34 | £79.25 |

| Couple (One or both 25+) | £666.97 | £100.05 |

3. The 2026 Bank Monitoring Rule: Which 15 Banks?

Under the Eligibility Verification Measure (EVM), banks are not “spying” on your daily coffee purchases. Instead, they run automated checks for two specific “eligibility indicators”:

- Capital Limits: Accounts holding more than the £16,000 threshold for means-tested benefits.

- Overseas Stays: Accounts used abroad for longer than the permitted period (usually 4 weeks).

The “DWP 15” Banks List

The vast majority of claimants bank with these 15 institutions, all of which are participating in the 2026 data-sharing rollout:

- Barclays, Bank of Scotland, HSBC, Halifax, Lloyds Bank, Metro Bank, Monzo, Nationwide, NatWest, RBS, Santander, Starling, TSB, Yorkshire Bank, and the Co-op.

The “Human-in-the-Loop” Safeguard: A bank flag does not mean your money is automatically stopped. A DWP officer must manually review the data before any deduction or suspension occurs.

4. Direct Deduction Orders (DDOs): Can they take money from your bank?

Previously, the DWP could only take money from your bank account by getting a Third Party Debt Order through a court—a slow and expensive process.

In 2026, the DWP can issue a Direct Deduction Order (DDO) directly to your bank. This is primarily used for people who:

- Owe a benefit debt but are no longer claiming benefits.

- Are not in PAYE employment (so a “Direct Earnings Attachment” isn’t possible).

- Have refused to engage with voluntary repayment plans.

SME/Self-Employed Note: If you are a sole trader, the DWP can issue a DDO against your business account if it is in your name. However, they cannot leave you with less than a “protected minimum balance” to cover essential living costs and business survival.

5. Driving Licence Suspensions: The Final Sanction

One of the most controversial parts of the 2025 Act is the power to suspend driving licences for benefit debt. This is not for “accidental” overpayments. It is a “last resort” for those who:

- Owe £1,000 or more.

- Have the clear means to pay (proven by bank monitoring).

- Have deliberately evaded all contact for repayment.

The Loophole: A court cannot suspend your licence if you can prove an “essential need” to drive. This includes needing your car for work (vital for SME owners), caring for a disabled relative, or living in an area with no public transport.

6. How to Challenge an Unaffordable Deduction

If a DWP deduction is leaving you unable to pay for food or rent, you have a legal right to request a Hardship Revision.

- Contact DWP Debt Management: Call 0800 916 0647.

- Provide Evidence: You will need to show a “Common Financial Statement” or recent bank statements proving your outgoings exceed your income.

- Ask for a Deferral: In 2026, the DWP can “pause” repayments for up to 3 months in exceptional circumstances.

FAQ

Can the DWP see my partner’s bank account?

Yes, if you claim as a couple. The DWP considers the “household” capital. If your partner has an account at one of the 15 banks, it will be checked against the joint £16,000 limit.

Does the DWP monitor the State Pension?

No. The 2026 monitoring powers explicitly exclude those only receiving the State Pension. These powers target means-tested benefits like Universal Credit, Pension Credit, and ESA.

What happens if the DWP makes a mistake?

Under the new Code of Practice, you have 28 days to make “representations” before a Direct Deduction Order takes effect. You also have the right to appeal to a First-tier Tribunal.

Can they take money from my wages and my bank at the same time?

No. DWP policy is to use one primary method of recovery. If you are in PAYE employment, they will almost always use a Direct Earnings Attachment (DEA) from your salary rather than a bank deduction.

Conclusion: The “Engagement” Strategy

The 2026 rules are designed to catch those who “can pay but won’t pay.” For the average claimant or small business owner, the best protection is early engagement.

If you receive a letter about an overpayment, do not ignore it. Agreeing to a voluntary repayment of even £5 a week prevents the DWP from using their more aggressive powers, such as Direct Deduction Orders or driving licence applications.

2026 Claimant’s Rights Checklist: Protecting Your Bank Account

If you have been notified of a DWP debt or a potential bank account deduction, use this checklist to ensure your rights are being upheld under the latest 2026 rules.

Phase 1: Verification & Transparency

- Request the Evidence: You have the right to a “Written Statement of Reasons.” If the DWP flags your bank account, they must explain which “eligibility indicator” (e.g., capital over £16k or overseas stay) triggered the review.

- Verify the “Human in the Loop”: Under the 2025 Act, an automated bank flag cannot result in an automatic deduction. Confirm with the DWP that a human officer has reviewed your case before any money is taken.

- Check the 15% Cap: Ensure the total deduction from your Universal Credit Standard Allowance does not exceed 15%. (Exception: This can rise to 25% only if fraud is proven).

Phase 2: Challenging the Deduction

- Request a “Hardship Revision”: If the deduction leaves you unable to pay for “essential living expenses” (food, rent, or heating), you can apply for a lower repayment rate.

- The 28-Day Representation Rule: If the DWP intends to issue a Direct Deduction Order (DDO) to your bank, they must usually give you 28 days to make “representations” (provide your side of the story) before the money is moved.

- SME Asset Protection: If you are a business owner, check if the DWP is counting “active business assets” as personal savings. You have the right to have these assets disregarded if your business is still trading.

Phase 3: The Appeals Process

- Mandatory Reconsideration (MR): You must ask for an MR within one month of a decision. In 2026, you can do this via your Universal Credit Journal or by calling the DWP Debt Management line.

- Independent Tribunal: If the MR fails, you have the right to an independent tribunal (HMCTS). This is a legal hearing separate from the DWP where an independent judge reviews the facts.

- Protect Your Driving Licence: If the DWP threatens a licence suspension, prepare evidence of “Essential Need.” If you need your car for work, childcare, or caring for a disabled relative, the court has the power to refuse the suspension.

Important Contacts for 2026

- DWP Debt Management: 0800 916 0647

- Pension Service Helpline: 0800 731 0469

- Universal Credit Helpline: 0800 328 5644