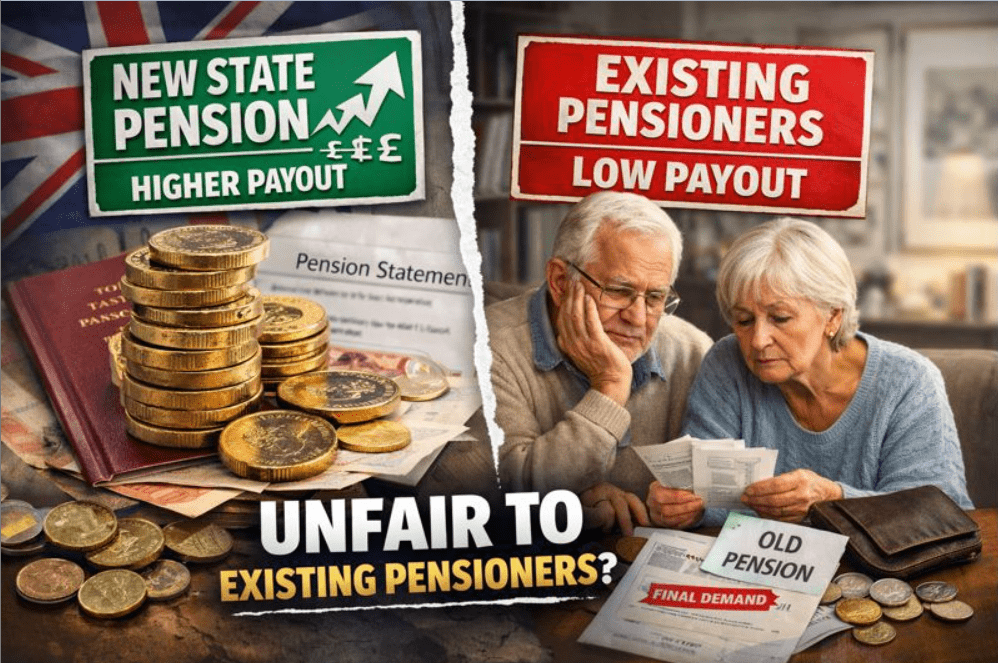

Is the New State Pension Unfair to Existing Pensioners? A Clear UK Guide to the Rules and What You Can Do

If you’ve ever thought the new state pension unfair to existing pensioners, you’re not alone. This topic sparks real frustration because people compare weekly amounts with friends, spouses, neighbours, or headlines, and the numbers don’t seem to line up.

Here’s the clear, straightforward answer: The new State Pension isn’t usually unfair to existing pensioners, it’s a different set of rules for different groups.

If you reached State Pension age before 6 April 2016, you’re normally paid under the old system (basic State Pension plus any Additional State Pension you earned, such as SERPS/S2P).

If you reached State Pension age on or after 6 April 2016, you’re normally paid under the new system (a flat-rate-style pension based on your National Insurance record, with transitional protections).

In practice, some existing pensioners receive less than the full new State Pension, but some receive more, mainly because the old system could include Additional State Pension.

Let’s explore exactly why this feels unfair, what’s actually happening, and what you can do if you suspect your amount is wrong or could be improved.

New State Pension Unfair to Existing Pensioners? A Clear UK Guide

The unfair feeling usually starts with a simple comparison:

- You (or a relative) receive something close to the basic State Pension.

- Someone else receives the full new State Pension.

- The weekly gap looks like you’re being penalised for retiring earlier.

The key point: the old system wasn’t just one number. It had layers. Many people on the old system receive basic State Pension plus Additional State Pension, which can lift their total above what the basic rate suggests. Others have little Additional State Pension (often linked to contracting out), so their amount looks lower.

What counts as an existing pensioner in State Pension terms?

Existing pensioner usually means you reached State Pension age before 6 April 2016 and are therefore under the old rules.

If you reached State Pension age on or after that date, you’re under the new rules, even if you worked for decades under the old system. That’s why the 2016 change is often misunderstood: it didn’t erase history; it built transitional rules on top of it.

If you’re also trying to make sense of how the timetable has shifted over the years, UK State Pension Age Retirement Changes adds context on why the date you reached State Pension age matters so much.

Old vs new State Pension at a glance

| Topic | Old system (reached State Pension age before 6 April 2016) | New system (reached State Pension age on/after 6 April 2016) |

| What it is | Basic State Pension plus possible Additional State Pension (SERPS/S2P) | Mostly single-rate pension based on NI record, with transitional protection |

| Why totals differ | Earnings-related add-ons could be significant | A starting amount in 2016 + the ability to build more after 2016 |

| Contracting out impact | Often reduces the Additional State Pension you’d otherwise have earned | Can reduce what you build towards the maximum (via your 2016 starting amount) |

| Can people get more than the headline full rate? | Yes (basic + Additional State Pension) | Yes, in some cases, via a protected payment |

New state pension unfair to existing pensioners: why comparisons feel unfair in real-life situations

Most this is unfair stories fall into one of these patterns:

- Comparing a full new State Pension to a basic-only old State Pension

If you compare the new system’s headline maximum to someone’s basic pension without considering the Additional State Pension, the comparison is lopsided.

- Contracting out creates a missing piece feeling

People who were contracted out often see a lower State Pension forecast/amount and assume they’ve lost money, without realising some value was redirected into workplace or private pension benefits.

- The 2016 starting amount is confusing

The new system starts with a 2016 baseline calculation and then allows post-2016 years to increase the amount. Two people with similar years can still get different outcomes because their pre-2016 histories differ.

Here’s what each of those means, in a way that helps you check your own position.

How the new State Pension works in depth

If you’re under the new system, your State Pension is not simply years × a rate. It’s a two-stage journey:

- A 2016 calculation creates your ‘starting amount’

- Post-2016 qualifying years can increase it (until you hit the maximum)

The 2016 starting amount — explained plainly

In 2016, the government worked out your starting amount using two different calculations based on your National Insurance record up to 5 April 2016:

- Old rules calculation: what you would have built up under the old system up to that point (basic + Additional State Pension, adjusted for contracting out).

- New rules calculation: what you would have built up if the new system rules had existed throughout your working life up to that point.

Your starting amount became the higher of those two. That higher of two calculations is why some people start quite close to the maximum, while others start much lower, even with a long work history.

Why 35 years doesn’t guarantee the full amount

You’ll often hear: You need 35 qualifying years for the full new State Pension.

That’s broadly true for someone whose record fits neatly into the new system logic, but if you have pre-2016 history (which most people do), especially with contracting out, the reality can be:

- You might need more than 35 years to reach the maximum.

- You might reach the maximum with fewer than 35 years.

- Your amount might not rise as expected because the 2016 starting amount already used your pre-2016 history in a specific way.

This is one of the biggest reasons people conclude it’s unfair: the rule-of-thumb gets repeated more often than the actual mechanism.

Protected payment – why some people can exceed the full new rate

If your 2016 starting amount was higher than the full new State Pension level, the excess can be kept as a protected payment on top of the new State Pension.

This is crucial for fairness debates: it shows the reform included transitional protection, so people didn’t automatically lose what they’d already built up.

Contracting out: the #1 reason people feel short-changed

Contracting out is where many unfair stories come from, and it’s easy to see why. The language is technical, and the result is emotionally simple: My State Pension is lower than I expected.

What contracted out actually means

For many years, some employees were allowed to be contracted out of the earnings-related part of the State Pension (Additional State Pension). This often applied if you were in certain workplace pension schemes.

The trade-off was typically:

- You and/or your employer paid lower National Insurance contributions, and

- Your workplace pension scheme was expected to provide benefits that replaced the State Pension earnings-related part you’d otherwise have built.

So it’s not that the money vanished. It often shifted, but not always in a way that’s obvious when you look only at your State Pension figure.

COPE: the label that causes confusion

You might see COPE (Contracted-Out Pension Equivalent) mentioned alongside your State Pension information. The easiest way to think about it:

- COPE is an estimate of the pension value you were expected to build in your contracted-out scheme instead of building the Additional State Pension.

Two important clarifications:

- COPE is not a bill you pay.

- COPE isn’t usually a line-by-line deduction you can reverse.

If you were contracted out, it’s normal that your State Pension may be lower than someone who was never contracted out, but you may also have higher workplace pension benefits than you otherwise would.

Where unfair can feel valid even if the rules were followed

Even if the system’s logic is consistent, contracting out can feel unfair when:

- You moved jobs often and lost track of scheme benefits.

- You’re comparing State Pension only (ignoring workplace pensions).

- Your contracted-out scheme benefits are smaller than you assumed.

- Communication at the time felt unclear or non-consensual (I didn’t choose this!).

So the fairness question isn’t always Were the rules followed? It can also be Did the overall outcome match reasonable expectations given the information people had?

If you’re on the old system, what it can include

If you reached State Pension age before 6 April 2016, you’re generally under the old system. The old system can include:

- Basic State Pension (based on your NI record), and

- Additional State Pension (SERPS/S2P) for people who built it up, and

- In some cases, inherited elements from a spouse/civil partner (rules vary and can be complex).

This is why two existing pensioners can receive very different amounts:

- One may have built a substantial Additional State Pension.

- Another may have little Additional State Pension (often linked to contracting out).

In other words, existing pensioners don’t automatically mean stuck on a lower rate. Many existing pensioners receive totals that compare favourably, sometimes even exceeding the full new State Pension.

Real-life scenarios (so you can place yourself quickly)

Scenario A: You’re an existing pensioner, and your amount looks lower than friends on the new system

This often happens when:

- Your pension is close to the basic State Pension level, and

- You have a little Additional State Pension on top.

That can be perfectly normal under the old rules, especially if contracting out reduced Additional State Pension accrual.

Scenario B: You’re an existing pensioner and your total is higher than the full new State Pension

This usually happens when:

- You earned a meaningful Additional State Pension (SERPS/S2P),

- You were not contracted out for much (or at all), and/or

- Your earnings history built a strong earnings-related entitlement.

Scenario C: You’re under the new system and your forecast seems stuck below the full amount

This often traces back to:

- Contracting out history affecting the 2016 starting amount,

- NI gaps, or

- A misunderstanding that 35 years guarantees full when the starting amount mechanism says otherwise.

These scenarios are why the keyword question keeps showing up: without this context, the system looks random. It isn’t random, but it isn’t intuitive either.

New state pension unfair to existing pensioners: a step-by-step guide to checking if yours is correct

Let’s make this practical. The goal is simple:

- Confirm whether your amount is correct.

- Identify whether you can increase it (if you’re not yet at the maximum under your scheme).

- Spot red flags that suggest an error rather than a rule difference.

Step 1: Identify which system you’re in

- If you reached State Pension age before 6 April 2016 → old system.

- If you reached State Pension age on/after 6 April 2016 → new system.

This single step prevents weeks of confusion, because advice differs depending on the scheme.

Step 2: Check your National Insurance record for gaps

Your NI record drives everything: qualifying years, missing years, and credits.

Common reasons for gaps:

- Periods abroad.

- Low earnings years.

- Self-employment with incomplete contributions.

- Career breaks, caring responsibilities, or administrative mismatches.

If you had caring responsibilities, for example, children or certain care roles, it’s especially worth confirming your credits were recorded correctly.

People often assumethe State Pension is purely about paid work, but the system can still recognise certain periods through credits and other rules.

If you’re thinking about entitlement where employment history is limited, how much State Pension will I get if I have never worked is a helpful reference point for how the UK framework treats non-working years.

Step 3: If you’re under the new system, understand whether you can still build more

Under the new system, extra qualifying years after 2016 can increase your amount, but only up to the maximum unless a protected payment applies.

If your record suggests you can increase it, that’s where the biggest wins are found: correcting missing years or deciding whether to fill gaps.

Step 4: If contracting out applies, compare total retirement income (not just the State Pension)

If you were contracted out, the State Pension alone will not tell the full story. One more thing that catches people out is that “fairness” isn’t only about the pension amount, it’s also about what you actually keep once tax is considered, especially if you have other retirement income on top.

If you’re reviewing the bigger picture, Alan Perkins State Pension Tax covers how State Pension tax works in practice and why two people with similar weekly payments can still feel very differently about the outcome.

You want to review:

- Your workplace pension scheme statements (especially for defined benefit schemes),

- Any preserved pensions from older employers,

- And whether your scheme includes contracted-out replacement benefits.

This is where many unfair stories resolve into: Ah, it’s in a different pot.

When voluntary NI contributions might help and when they won’t

Voluntary NI contributions can be powerful, but only when they actually increase your entitlement.

They tend to be worth considering if:

- You’re under the new system.

- Your record shows missing years.

- And you’re not already forecast to reach the maximum without paying.

They tend not to be worth it if:

- You’ll hit the maximum anyway through future qualifying years, or

- Paying for a missing year doesn’t increase your pension (because of how your starting amount works), or

- There are cheaper/free routes via NI credits you should claim first.

This is a classic measure twice, cut once situation. The best approach is to focus on the outcome: Will paying for this year increase my weekly pension, and how long will it take to break even?

Feels unfair? Likely explanation and what to do next

| What you notice | Likely explanation | What you can do next |

| My friend gets the full new State Pension; I don’t. | Different systems (pre/post-2016) or different NI histories | Confirm which system you’re in; compare like-for-like |

| I’ve got 35 years but not the full new amount. | 2016 starting amount + contracting out can change the math | Check whether more post-2016 years increase your amount |

| My forecast mentions contracting out / COPE. | Part of the entitlement built in workplace scheme instead | Pull workplace scheme paperwork; view total retirement income |

| My NI record has gaps I don’t recognise. | Missing contributions/credits or admin mismatch | Gather payslips/P60s/care evidence; pursue corrections |

| My pension seems too low given my life history. | Could be rules, or could be error/underpayment | Treat as a verification task, not just a fairness debate |

The myths that keep this debate going and the truth

- Myth: Existing pensioners are always worse off.

- Truth: Many existing pensioners receive Additional State Pension on top of the basic amount, so totals can be higher.

- Myth: COPE is a deduction I can reclaim.

- Truth: COPE is an estimate linked to contracted-out history; it reflects pension built elsewhere rather than a simple “charge”.

- Myth: 35 years guarantees the full new State Pension.

- Truth: For people with pre-2016 history, the 2016 starting amount mechanism can change what’s needed.

That’s the foundation for most misunderstandings. Once you see these clearly, the system looks less like a penalty and more like a complex transition.

When unfair may actually mean wrong: signs you should investigate underpayment or errors

It’s completely possible for the system to be applied correctly and still feel unfair, but it’s also true that errors happen.

Consider investigating more deeply if:

- Your NI record misses years you can clearly evidence.

- Caring responsibilities or credits don’t appear where expected.

- Your marital/civil partnership history suggests inheritance rules might apply under the old system,

- Your pension amount changed unexpectedly without a clear explanation.

- Or you’ve received letters indicating historic underpayment exercises (some groups have been affected more than others).

Here’s what you can do next: treat your case like an audit. Gather documents, list specific years and events, and approach the issue as My record may be incomplete rather than The system is unfair.

That change in framing often leads to faster, more productive outcomes.

Complaints and corrections: how to challenge your amount without getting bounced around

If you believe your amount is wrong, the fastest route is to be specific.

- Write down your core point in one sentence: “I believe my State Pension is incorrect because I have missing NI years or credits, my contracted-out history may not be reflected correctly, or inheritance rules may not have been applied.”

- Create a simple timeline:

- employment periods.

- self-employment periods.

- caring periods.

- periods abroad.

- Gather proof for the years in dispute:

- P60s/payslips.

- letters confirming benefits/credits.

- employer confirmation.

- childcare/care-related evidence if relevant.

- Ask for a review with clear questions:

- Which years are not counted as qualifying, and why?

- Is my contracted-out history included in the calculation?

- Under which rules am I being paid (old/new), and what components make up my weekly amount?

If you do this, you steer the conversation away from generic scripts and towards a checkable calculation.

A clear fairness lens: legal fairness vs political fairness vs personal fairness

It helps to separate three different meanings of unfair:

- Legal/administrative fairness: Were the rules applied correctly to you?

- Political fairness: Should the government equalise outcomes across groups, even if they accrued under different rules?

- Personal fairness: Does your outcome match what you reasonably expected after decades of contributions?

Most people asking new state pension unfair to existing pensioners are really asking about personal fairness. But the fix often sits in legal/administrative fairness first: “Is my record accurate, and am I receiving what I’m entitled to?”

It’s also worth noting that some fairness debates aren’t just about comparing old versus new systems; they’re about wider retirement policy impacts on particular groups.

For example, campaign conversations around notice periods and the pace of change are often referenced in discussions like Women Against State Pension Inequality, which helps explain why “unfair” can mean different things to different readers depending on their life and work history.

Once entitlement is confirmed, the political debate becomes: “Should outcomes be harmonised?” That’s a much bigger question, and it’s why reforms often include transitional protections rather than retrospective equalisation.

What people speak about this online?

State pension triple lock was described as ‘silly system’… by new pensions minister

byu/JayR_97 inukpolitics

Why is the state pension so unfair? A reader asks why his state pension is so much lower than his younger friend’s just because of their dates of birth. The gap between new and old state pensions rises to £51.70 a week from April https://t.co/efnLiPF5W0 my Money Clinic @theipaper

— Paul Lewis (@paullewismoney) March 20, 2024

Final summary (what to remember and what to do next)

- The new State Pension is not usually unfair to existing pensioners; it’s a different rulebook applied to different cohorts.

- Existing pensioners can receive the Additional State Pension, which means many totals are not directly comparable to the new system’s flat-rate maximum.

- Contracting out is a major driver of lower State Pension figures for some people, but it often links to benefits built in workplace schemes instead.

- If your numbers look wrong, don’t stop at unfair; verify your NI record, your scheme status, and your calculation components.

Also, if you live abroad (or plan to), “fairness” can take on another angle because the uprating rules aren’t the same everywhere.

Some people discover that their State Pension increases each year in one country but not in another, which can significantly change long-term outcomes even when the starting amount is identical.

If that’s relevant to you, Frozen State Pension News explains how uprating works and why location can affect what you receive over time.

Here’s what you can do next:

- Confirm which system you’re in (pre/post-6 April 2016).

- Check your NI record for gaps or missing credits.

- If under the new system, see whether more qualifying years will increase your amount.

- If contracting out applies, review workplace pension benefits to understand the full picture.

- If anything doesn’t add up, challenge it with a timeline and evidence

FAQs

Is COPE deducted from my State Pension?

COPE is an estimate linked to contracted-out history. It reflects that part of your pension value was expected to be built in a workplace scheme instead of in the earnings-related State Pension component. It’s not usually a simple deduction you can reclaim.

Can I top up my State Pension after retirement?

Sometimes. It depends on your record and whether filling missing years will actually increase your entitlement. Always check the expected outcome first, so you don’t pay for a year that won’t raise your pension.

Why do some people get more than the full new State Pension?

Existing pensioners may receivethe Additional State Pension on top of the basic amount. Under the new system, some people can also have a protected payment on top of the standard maximum due to transitional rules.

How do I know if my State Pension is correct?

Treat it like a verification process: confirm which system you’re in, review your NI record, understand whether contracting out applies, and ask for a component breakdown if anything looks inconsistent.